2020 State of the Industry Report

Six industry experts focus on the future of composites.

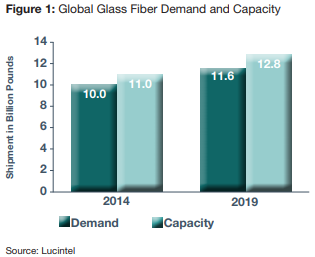

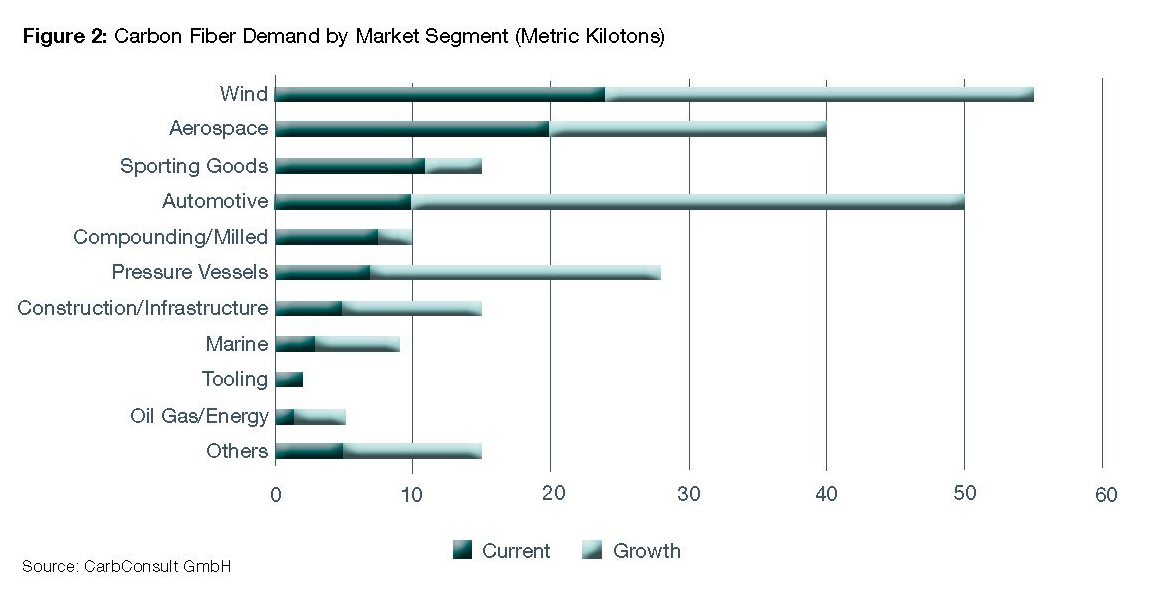

In 2019, Composites Manufacturing magazine covered innovations throughout the industry, from experimental wind turbines and structural composites on electric vehicles to 3D tooling and automated manufacturing operations. The editorial team is excited to see what’s in store for 2020. We kick off the New Year with our annual State of the Industry report, looking at key materials and markets in the industry. The Glass Fiber Market By Sanjay Mazumdar, CEO Lucintel Against the backdrop of unresolved U.S./China trade disputes, the U.S. composites industry remains positive and continues to show growth, driven particularly by the wind energy, aerospace and construction industries. Overall, the U.S. composite end products market was valued at $26.7 billion in 2019 and is forecast to grow at 3.8% compound annual growth rate (CAGR) in the next five years to reach $33.4 billion in 2025. Glass fiber-based composites dominate the market, followed by carbon fiber-based composites. In the U.S., glass fiber is a major reinforcing material, growing by 1.7% in 2019 and reaching 2.6 billion pounds in terms of volume and $2.2 billion in terms of value. The glass fiber demand for the U.S. is expected to reach 3 billion pounds by 2025 with a CAGR of 2.4%. Owens Corning, Jushi, Nippon Electric Glass, CPIC and Johns Manville are some of the top suppliers of glass fiber in the U.S. The glass fiber industry is quite consolidated, with the top three companies accounting for more than 50% of the total output by value. The main consumers of glass fiber in the U.S. are the transportation (including automotive), construction, and pipe and tank segments. Together, they represent 69% of the total usage. Future trends indicate that these key sectors offer significant growth potential for the U.S. composites industry. Increasing residential and commercial construction, continuous growth in oil and gas activities and water/wastewater infrastructure, and rising demand for lightweight vehicles are expected to drive this market. The transportation market, which includes buses, coaches, commercial vehicles and automobiles, is expected to be one of the biggest U.S. markets in the next five to 10 years. Key vehicle manufacturers are investing in composite materials technology to reduce weight and meet the legislated carbon emission reduction targets. In the construction industry, common applications for GFRP include paneling, bathrooms and shower stalls, doors and windows. Glass fiber demand in construction registered 1.5% growth in 2019 in terms of value shipment. The growth is driven by a continuous increase in employment, low mortgage rates and slowing house price inflation. The continued easing of lending standards and increased funding support from state and local construction measures are other major drivers for the U.S. construction market. Due to climate change and the occurrence of natural calamities (like earthquakes and hurricanes), the major challenges facing U.S. infrastructure require strong research efforts and increased use of advanced technologies and materials. Composites are increasingly being used to repair and retrofit structures built with other materials. The pipe and tank market was flat in 2019 as oil and gas activities declined due to disruption by Hurricane Barry in the Gulf of Mexico and slow growth in oil demand. FRP pipes and tanks are not only used in oil and gas applications, but also have huge opportunities in chemical, industrial, water/wastewater and sewage applications. According to the Environmental Protection Agency, more than 40% of water pipelines are in poor to life-elapsed conditions and require correction (repairs for old pipes and installation of new pipes), which, in turn, will drive demand for FRP pipes. In terms of supply and demand, global glass fiber capacity was 12.8 billion pounds in 2019 and is currently running at 91% utilization. Lucintel predicts that the fiberglass plant capacity utilization will go down slightly to approximately 90% in 2020 as glass fiber producers add more production capacities. To fulfill the increasing demand for glass fiber in various applications, companies are trying to grow both organically and inorganically. In 2019, Jushi USA put its alkali-free fiber production line into operation with an annual capacity of 96,000 tons and a total investment of $350 million, whereas Nippon Electrical Glass acquired the remaining PPG USA fiberglass operations in 2017-18 with a value of $550 million. The Carbon Fiber Market By Daniel Pichler, Managing Director CarbConsult GmbH In 2019, demand for carbon fiber globally totaled approximately 100,000 metric tons. The market continues to grow at 10 to 12% per year, fueled by incremental volume gains in carbon fiber use in aerospace, wind turbine blades and several other industrial applications. Growth at this rate is likely to continue for the foreseeable future. The approximate breakdown of carbon fiber use by market segment is as follows:

The transportation market, which includes buses, coaches, commercial vehicles and automobiles, is expected to be one of the biggest U.S. markets in the next five to 10 years. Key vehicle manufacturers are investing in composite materials technology to reduce weight and meet the legislated carbon emission reduction targets. In the construction industry, common applications for GFRP include paneling, bathrooms and shower stalls, doors and windows. Glass fiber demand in construction registered 1.5% growth in 2019 in terms of value shipment. The growth is driven by a continuous increase in employment, low mortgage rates and slowing house price inflation. The continued easing of lending standards and increased funding support from state and local construction measures are other major drivers for the U.S. construction market. Due to climate change and the occurrence of natural calamities (like earthquakes and hurricanes), the major challenges facing U.S. infrastructure require strong research efforts and increased use of advanced technologies and materials. Composites are increasingly being used to repair and retrofit structures built with other materials. The pipe and tank market was flat in 2019 as oil and gas activities declined due to disruption by Hurricane Barry in the Gulf of Mexico and slow growth in oil demand. FRP pipes and tanks are not only used in oil and gas applications, but also have huge opportunities in chemical, industrial, water/wastewater and sewage applications. According to the Environmental Protection Agency, more than 40% of water pipelines are in poor to life-elapsed conditions and require correction (repairs for old pipes and installation of new pipes), which, in turn, will drive demand for FRP pipes. In terms of supply and demand, global glass fiber capacity was 12.8 billion pounds in 2019 and is currently running at 91% utilization. Lucintel predicts that the fiberglass plant capacity utilization will go down slightly to approximately 90% in 2020 as glass fiber producers add more production capacities. To fulfill the increasing demand for glass fiber in various applications, companies are trying to grow both organically and inorganically. In 2019, Jushi USA put its alkali-free fiber production line into operation with an annual capacity of 96,000 tons and a total investment of $350 million, whereas Nippon Electrical Glass acquired the remaining PPG USA fiberglass operations in 2017-18 with a value of $550 million. The Carbon Fiber Market By Daniel Pichler, Managing Director CarbConsult GmbH In 2019, demand for carbon fiber globally totaled approximately 100,000 metric tons. The market continues to grow at 10 to 12% per year, fueled by incremental volume gains in carbon fiber use in aerospace, wind turbine blades and several other industrial applications. Growth at this rate is likely to continue for the foreseeable future. The approximate breakdown of carbon fiber use by market segment is as follows:- Wind energy – 25%

- Aerospace – 20%

- Sporting goods – 10 to 12%

- Automotive – 10 to 12%

- Compounding for injection molded plastics – 5 to 8%

- Pressure vessels – 5 to 8%

- Construction and infrastructure – 5 to 8%

- Other market segments – 15%

There are other issues, too. For instance, the challenge of unlocking mass adoption of CFRP in every day automobiles produced in the millions goes beyond pure technical and economic considerations. Sustainability and recycling also need to be addressed. But these issues are being tackled up and down the value chain.

The Automotive Market

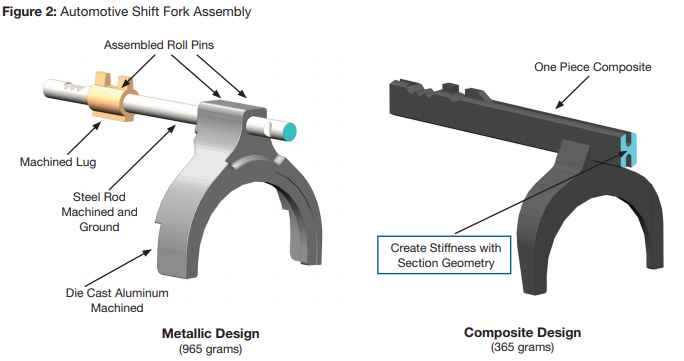

By Marc Benevento, President Industrial Market Insight Across the globe, light vehicles (gross vehicle weight rating under 8,500 pounds) consume roughly 5 billion pounds of composites on an annual basis. Thermoplastic matrix composites account for a majority of the volume. Composites and other lightweight materials have enjoyed strong growth recently, but the year ahead brings some headwinds for composites in automotive applications. The primary growth inhibitors will be a relatively flat market for light vehicles globally and a relaxation of fuel economy standards in the United States. However, opportunities for growth will exist as OEMs continue to reduce vehicle weight on global vehicle platforms. Suppliers of automotive materials will need to gain market share to grow in 2020 because very little year-over-year production growth is expected. Europe is forecast to be flat, and a slight decline is anticipated in NAFTA as well. China is expecting low single-digit growth, which is very modest when compared to the phenomenal annual growth observed recently. Since the global production outlook is 2 to 3% per year through 2025, suppliers of composites will need to earn market share from incumbent materials in order to find meaningful growth. In addition to general market sluggishness, relaxation of corporate average fuel economy standards in the United States will impact growth of composites in automotive. Weight reduction has been part of the OEM strategy to meet steadily increasing fuel economy and carbon dioxide emission regulations. These regulations have been the primary driver of the increased adoption of lightweight materials in automobiles over the past decade. With the United States proposing to hold fuel economy regulations flat through 2026, OEMs will have less incentive to invest in weight-saving materials such as composites. This is particularly true for pickup trucks and large SUVs that are sold primarily in the United States. Suppliers of composites and other lightweight materials should expect less interest on U.S.-specific platforms given the current regulatory environment. Rollbacks of fuel economy standards in the U.S. are only a minor setback to the adoption of lightweight materials on automobiles globally. More stringent regulation of carbon dioxide emissions outside of the U.S. will continue to drive the need for vehicle weight reduction on global vehicle platforms. Furthermore, weight reduction is critical to extend the range of battery-electric vehicles, and the pursuit of lightweight materials will continue for this small, but growing segment. Interest in composites for vehicle weight reduction will persist despite the “pause” on U.S. fuel economy regulations.In order to capitalize on this interest, composite part suppliers will have to sharpen their value proposition versus alternative offerings. High-strength steel and aluminum have been the biggest beneficiaries of OEM weight reduction efforts in North America over the past decade, gaining 6% and 3% of vehicle mass, respectively. This share has been taken primarily from mild steel, which is the baseline automotive grade steel from the standpoint of cost, manufacturability and strength-to-weight ratio.

Like glass fiber, the carbon fiber industry also has undergone restructuring and optimization, with several carbon fiber companies declaring bankruptcy last year. The driving applications for CFRP in China are within the wind energy industry, electricity transmission, electric vehicles, the 3Cs (computers, cell phones and communications, including 5G), sports and city transit. Overall, the composite industry in China faces strict environmental regulations, price increases in chemical and raw materials, cost increase in labor and rising energy costs. Achieving competitiveness through innovation is key. For example, traditional hand lay-up manufacturing has been gradually phased out in China. Currently, there is a need for advanced manufacturing equipment, including closed molding technologies. Automation will also become a necessity to make operations more competitive. In 2019, the U.S./China trade war worsened, and it appears it may not end soon. Multilateral trade, including China-EU trade, is affected, and global trade tensions are escalating. At present, fiberglass, carbon fiber, basalt fiber and all composite products have been included in the United States plus-25% tariff list. These global trade uncertainties have forced the Chinese composites industry to expand domestic markets. In conclusion, the future healthy growth of the Chinese composites industry will rely more on scientific and technological innovation and product quality improvement, rather than on resources, low-cost labor and an expanding production capacity. New initiatives from the government related to rural area construction, modern agriculture and farming, and 5G communications will expand existing applications and open up new ones for composite materials and structures. Looking ahead, composites have a bright future in China. Thanks to Changlei Liu of the China Fiberglass Industry Association and Professor Jian Xu of Shenzhen University for contributions to this section.

Like glass fiber, the carbon fiber industry also has undergone restructuring and optimization, with several carbon fiber companies declaring bankruptcy last year. The driving applications for CFRP in China are within the wind energy industry, electricity transmission, electric vehicles, the 3Cs (computers, cell phones and communications, including 5G), sports and city transit. Overall, the composite industry in China faces strict environmental regulations, price increases in chemical and raw materials, cost increase in labor and rising energy costs. Achieving competitiveness through innovation is key. For example, traditional hand lay-up manufacturing has been gradually phased out in China. Currently, there is a need for advanced manufacturing equipment, including closed molding technologies. Automation will also become a necessity to make operations more competitive. In 2019, the U.S./China trade war worsened, and it appears it may not end soon. Multilateral trade, including China-EU trade, is affected, and global trade tensions are escalating. At present, fiberglass, carbon fiber, basalt fiber and all composite products have been included in the United States plus-25% tariff list. These global trade uncertainties have forced the Chinese composites industry to expand domestic markets. In conclusion, the future healthy growth of the Chinese composites industry will rely more on scientific and technological innovation and product quality improvement, rather than on resources, low-cost labor and an expanding production capacity. New initiatives from the government related to rural area construction, modern agriculture and farming, and 5G communications will expand existing applications and open up new ones for composite materials and structures. Looking ahead, composites have a bright future in China. Thanks to Changlei Liu of the China Fiberglass Industry Association and Professor Jian Xu of Shenzhen University for contributions to this section. The European Market

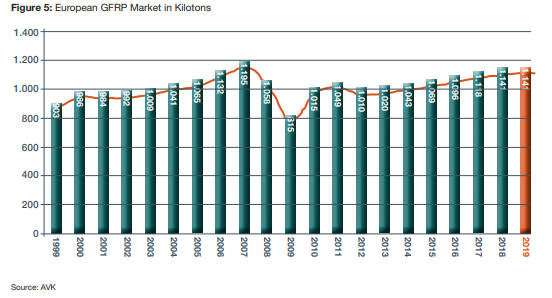

By Elmar Witten, Managing Director AVK, the German Federation of Reinforced Plastics After six successive years of modest growth, European GFRP production remained steady in 2019 at a total volume of 1.14 metric tons. The stagnation did not affect all areas equally. Some growth occurred in thermoplastic processes, sheet molding compound (SMC)/bulk molding compound (BMC), resin transfer molding (RTM) and pultrusion. In addition, some eastern European countries and Turkey expected growth in 2019. Overall, glass fiber remained the dominant material by far, used for reinforcement in more than 95% of the total volume of composites. Global demand for CFRP was estimated at 141,500 metric tons in 2019, or 1% to 2% of the market. The two main market segments for GFRP in Europe remain construction/infrastructure and transportation, each accounting for approximately one-third the total production volume. For the first time in many years, the construction/infrastructure market segment is now a larger consumer of GFRP at 36% of the total European market compared to the transport sector (34%). The two other areas with significant market share in 2019 were electric/electronics at 15% and sports/leisure at 14%. In recent years, GFRP production has grown more slowly in Europe than in America and Asia. Reasons for this sluggish growth include the migration of certain manufacturing processes and methods, as well as outsourcing of the production of commodities with often low-profit margins. In addition, some specific applications and customer industries, such as automotive, are growing more dynamically in other regions of the world than in Europe. The automotive sector, one of the central pillars of the composites industry, is now undergoing a massive transformation with changing material requirements, new challenges in drive technology and construction and innovations such as autonomous driving systems. Countries with large export surpluses in this sector, such as Germany, are hardest hit by any slow-down in the market. This affects not only OEMs, but the entire supply chain, including composites fabricators and material suppliers. It’s important to note that market trends within Europe vary widely from country to country. While the overall market stagnated year-on-year at 1.14 metric tons, growth rates in Europe ranged from -2.55% to +4.35%. The largest European country in the GFRP/composites market continues to be Germany, with a total production volume of 225,000 metric tons (down 1.75% from 2018). Only Eastern European nations registered growth last year. Production in the United Kingdom, Ireland, Austria and Switzerland was stable. All other countries anticipated production to fall in 2019. The overall mood within the composites sector is subdued, fueled by growing stock market uncertainty, declining rates of investment and a generally turbulent economic climate. The gross domestic product (GDP) indicators for Europe as a whole – and many of its national economies – are currently starting to turn downward. The market is also adversely affected by growing political uncertainties within the European Union and in international trade. Brexit, trade disputes between the United States and China and the protectionist policies of various countries are creating insecurity. Despite these challenges to the European composites industry, there is promise. Some areas show tremendous potential, such as construction of the 5G network and renovation of bridges and buildings. However, awareness of composite materials is still too low for them to be widely considered by end user decision-makers. This must change because composites are a good, if not better choice for many applications. If customers can reassess these materials and composites become subject to standards/norms, then market growth is assured for years to come.

Vectorply combines highly engineered composite reinforcements w/ industry-leading engineering & technical support to help customers achieve their production goals.

A lower-cost “print only” line of machines built around proven LSAM technology

More from Composites Magazine

SUBSCRIBE TO CM MAGAZINE

Composites Manufacturing Magazine is the official publication of the American Composites Manufacturers Association. Subscribe to get a free annual subscription to Composites Manufacturing Magazine and receive composites industry insights you can’t get anywhere else.