2021 State of the Industry Report

At the start of 2020, composites industry pundits couldn’t have predicted the impact a global pandemic would have on the market. The U.S. composites industry showed signs of growth, but was soon derailed by plant closings, employee layoffs and postponed projects in response to COVID-19. However, composites professionals are resilient and by the end of last year, signs pointed to a steady recovery. In our 2021 State of the Industry Report, five experts share their expectations for key materials and markets.

The Glass Fiber Market

By Dr. Sanjay Mazumdar, CEO, Lucintel

2020 was a crisis management year for composites industry players due to COVID-19, which caused a cash flow and demand crisis, supply chain disruptions and worker safety issues. While last year was challenging, the outlook appears brighter for 2021.

At the beginning of 2020, the U.S. composites industry started fairly well and showed good signs of growth similar to 2019. By the end of March, new orders were delayed and sometimes canceled. During the second quarter, particularly in April and May, the impact of the pandemic was at its greatest, resulting in one of the sharpest and deepest economic contractions since the Great Depression. More than 20 million people lost jobs in the summer, and plants were shut down across sectors. Transportation, construction and marine were hit the hardest, which resulted in a 20% decrease in demand for U.S. glass fiber in Q2 2020 compared to Q1 2020. The impact of COVID-19 was reflected in the financial results of many composites industry players during the first half of 2020 in terms of poor sales and profit margins.

However, the second half of 2020 saw one of the fastest recoveries in the economy and the composites industry. Since July 2020, the U.S. composites industry has started to see an increase in demand from various end-use industries, including automotive, marine and construction, driven by stimulus packages and plant re-openings. As a result, the U.S. glass fiber market grew by approximately 23% in Q3 2020 compared to Q2 2020. In Q4 2020, the U.S. glass fiber market remained strong, and November saw approximately 5% growth compared to November 2019.

By the end of 2020, the glass fiber market could not recover fully from the dent of the pandemic and was expected to witness a decline of about 6%, with demand dropping to 2.44 billion pounds compared to 2.59 billion pounds in 2019. The impact of the coronavirus was irregular across value chains, with automotive, pipe and tank, aerospace and marine applications experiencing significant declines, while wind energy, electrical and electronics, and construction remained positive.

The wind industry provided a bright spot in 2020, witnessing double-digit growth despite a temporary slowdown in March and April due to supply chain bottlenecks, cross-border shipment issues and government restrictions. Overall, the market grew as wind farm developers were in a hurry to get construction started in time to qualify for the production tax credit before its expected expiration at the end of the year.

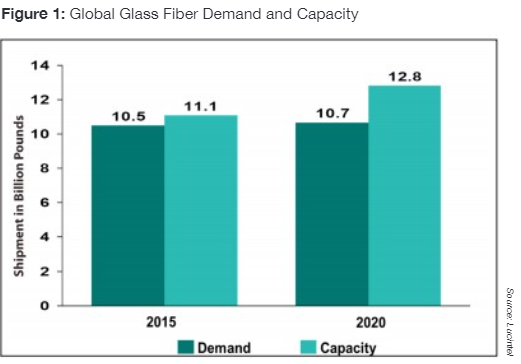

In terms of supply and demand dynamics in the glass fiber industry, the utilization rate decreased to 83% in 2020 from 91% in 2019. The global glass fiber capacity was 12.8 billion pounds in 2020. (See Figure 1.) Lucintel predicts that the fiberglass plant capacity utilization rate in 2021 will reach the same level as 2019.

COVID-19 is forcing executives to rethink the future of the composites industry. In some segments, there is a surplus capacity added to the slow recovery. For example, the aerospace industry will see a slow recovery. Boeing CEO Dave Calhoun estimates it will take two to three years for air travel to recover to pre-COVID levels.

There is also growing consumer awareness about sustainability, which has led industry players to explore green materials, renewable energy and recycling technologies in the production of materials and composite parts. In addition, the increased use of digital technologies in most sectors is transforming work and the workforce.

With the help of a new stimulus package approved in December and arrival of the coronavirus vaccine, Lucintel is hopeful that Q1 and Q2 2021 will see good recovery in the U.S. glass fiber industry. Favorable trends in automotive, housing, pipe and tank, electrical and electronics, consumer goods and marine post-COVID crises will lead the glass fiber market to grow at 8% to 10% in 2021 to reach or exceed 2019 level demand.

The Automotive Market

By Marc Benevento, President, Industrial Market Insight

Last year brought significant change and disruption to many industries and aspects of life. The automotive and composites industries were no exception, and both have been dramatically impacted by COVID-19, the effects of which will be felt for years to come. However, there is good news for composite manufacturers in that the expected automotive industry recovery, global regulatory environment and proliferation of electrified vehicles provide a promising outlook for composites and lightweight automotive materials.

COVID-19-related shutdowns dramatically and negatively affected light vehicle supply and demand in 2020. Manufacturing shut-downs early in the year brought demand for materials to an abrupt halt, and the economic impacts of the pandemic reduced demand for new passenger vehicles globally. Although production resumed by summer and demand recovered more quickly than anticipated, global production in 2020 was 20% below that of the prior year. The volume of composites sold in automotive applications fell commensurately, to about 3.5 billion pounds.

Recovery of light vehicle production will be gradual and with notable regional differences. China, a large developing market where the effects of the coronavirus were felt first, is expected to fully recover to 2017 levels by 2022. Vehicle demand in mature markets, such as the European Union and North America, was softening before the pandemic and will not return to 2017 levels before 2025. The road to recovery will be long and slow for suppliers of automotive commodities that rise and fall with the market.

Fortunately, many composite materials are not commodities, but are gaining market share due to the value they offer versus competing materials in terms of cost, weight and performance. Demand for lightweight materials is outpacing market growth due to regulations on carbon dioxide emissions and fuel economy. Limits on carbon dioxide emissions in Europe are set to tighten over 60% between 2021 and 2030.

The United States is likely to revisit the pause placed on Obama-era fuel economy standards, which could require a 23% improvement in fleet fuel economy between 2020 and 2025. The use of lightweight materials, including composites, can assist OEMs in meeting regulations while retaining consumer appeal. Prior efficiency regulations helped composites gain 2% of vehicle mass each year from 2008 to 2018, a trend that is likely to continue in light of the current regulatory environment.

However, lightweight materials alone will not enable OEMs to meet lofty fuel economy requirements. As a result, automakers are planning to deploy a new mix of electrified vehicle powertrains in the next few years. This will include significant increases in hybrid, battery electric and fuel cell vehicles to complement internal combustion engines.

The rise of electrified vehicles creates opportunities for composites in battery enclosures, hydrogen fuel tanks and other components where low weight and corrosion resistance are required. In addition, part consolidation opportunities can be exploited as these new vehicles are designed. These factors may enable composites to capture additional share of vehicle mass in the next decade and will help drive the total volume of automotive composites sold above 2017 levels by 2023.

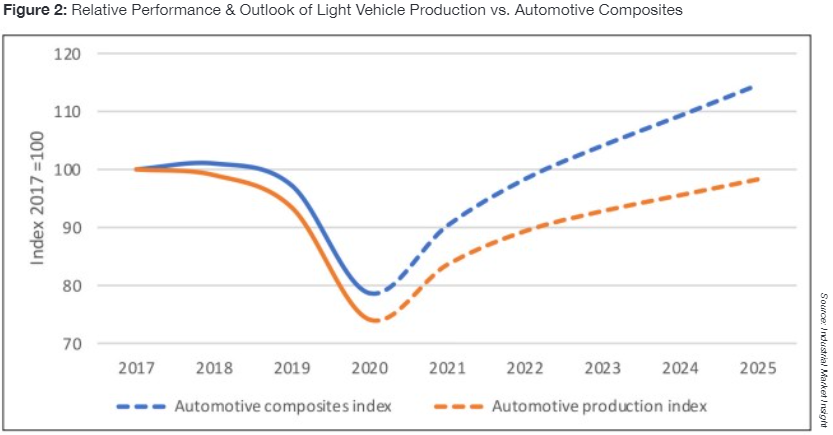

The growth potential of the composites industry is illustrated by indexing vehicle production and automotive composites volume to a base year of 2017 and projecting demand through 2025. (See Figure 2.) Should composites continue to grow 2% above the market each year, as they have for the past decade, automotive composites volume will eclipse the base year by 2023, while global automotive production is not expected to return to its 2017 level before 2025.

Although 2020 has been a difficult year for the automotive industry and composite manufacturers, the long-term outlook for automotive composites is bright. The industry will rise above 2017’s high water mark in the next few years based on the value offered in terms of cost, weight and performance.

The Carbon Fiber Market

By Daniel Pichler, Managing Director, CarbConsult GmbH

Since 2010, the market for carbon fiber has grown from less than 40,000 metric tons to more than 100,000 metric tons in 2019. Growth during this period was smooth and uninterrupted, with a 10 to 12% increase per year. But last year, the COVID-19 pandemic struck, and the carbon fiber world changed almost overnight.

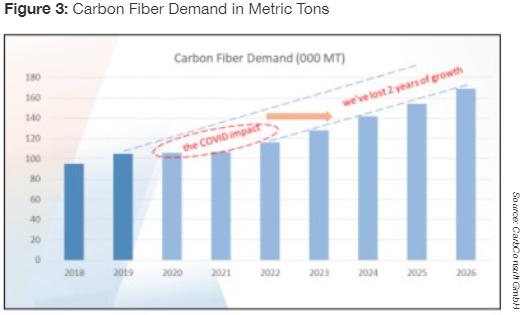

In 2020, global demand for carbon fiber totaled approximately 105,000 metric tons – just 1% higher than in 2019. And in 2021, only 1% growth is to be expected. (See Figure 3.) To understand the flattening of the market, it’s important to take a closer look at how COVID-19 changed the carbon fiber world.

The market for carbon fiber is fueled by growth in a number of areas, such as aerospace, wind energy, sporting goods, marine, automotive, pressure vessels and others. Until 2020, growth in all of these market segments individually and in the industry as a whole was steadily rising.

With borders shut in early 2020, international air travel stopped, aircraft were grounded, aircraft manufacturers slashed production rates and, in an instant, the carbon fiber industry lost its motor. Carbon fiber use in aerospace applications made up 20% or more of industry volume and 40% of industry value. The slowdown in commercial aerospace severely impacted the carbon fiber industry, and it will likely take several years to recover to pre-COVID levels.

Although the aerospace news was discouraging, not all news in 2020 was bad. As we learned to stay at home, work from home and holiday near home, some markets did well. Demand for sporting goods jumped 30% to 40% in 2020, and installations of wind turbines continued as planned 20% higher than in the previous year.

The breakdown of carbon fiber use by end-use market in 2020 was roughly as follows:

- Wind energy – 23%

- Aerospace – 20%

- Sporting goods, including marine – 12%

- Automotive – 10%

- Pressure vessels – 10%

- Compounding for injection molded plastics and other short fiber applications – 8%

- Construction and infrastructure – 8%

- Other market segments – 9%

As in pre-COVID times, all market segments for carbon fiber have significant potential for growth as new applications and programs come into production. The underlying long-term megatrends that made carbon fiber attractive before COVID-19 remain unchanged. The advantages carbon fiber offers – stiffness, high strength-to-weight performance, corrosion resistance, electrical conductivity and others – are still valid today. For growth to occur, carbon fiber and CFRP parts must demonstrate both technical and economic benefits.

So we have a mixed bag of individual industries and applications driving overall demand for carbon fiber – some down, some up in these COVID times. Those segments that have contracted – especially aerospace – caused the total carbon fiber industry to look relatively flat in 2020, with only very modest growth expected for 2021. However, there is a more favorable long-term outlook. In a couple of years, one can reasonably expect to see a return to more robust year-on-year growth in the carbon fiber industry once again.

As for the industry’s capacity to produce carbon fiber, industry nameplate capacity of carbon fiber producers collectively is approximately 160,000 metric tons – more than enough to satisfy demand in current times. And several producers are planning additional new plants and capacity to satisfy increased future demand.

Finally, we must keep in mind that carbon fiber is still an industry in its early development phase. Aircraft are hand-built at a rate of just one or two per day; other applications slightly higher, but still without automation. Automobiles, on the other hand, are mass produced at rates exceeding one per minute. Today, carbon fiber is still used mostly in low-volume applications. It has not yet robustly demonstrated “mass production.” Surely this will come, but when is not certain.

In summary, COVID has dealt the carbon fiber industry a blow, but it will be temporary. Despite the events of this extraordinary year, the future is promising for carbon fiber, and developments in the next couple of years will be interesting.

The Aerospace Market

By Dr. Terrisa Duenas, Chief Technology Officer, Nanoventures

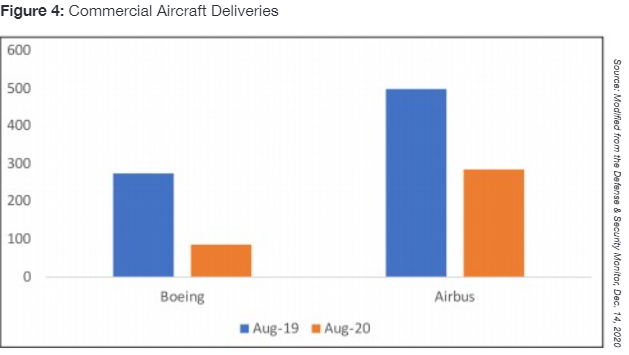

The aerospace industry has been affected dramatically by a confluence of events in the past couple of years, most notably the grounding of the Boeing 737 Max and the rise of the COVID-19 pandemic. On Nov. 18, 2020, FAA Administrator Steve Dickson rescinded the grounding order issued on March 13, 2019, of the Boeing 737 Max. But the intervening 18 months took a toll on the industry. In addition, both Boeing and Airbus had to temporarily close their facilities during the COVID-19 pandemic. As expected, both Boeing and Airbus struggle with significant cuts in production rates and lower orders. (See Figure 4.)

As the aerospace industry rebounds, technology solutions informed by innovation will be paramount to its success. Projects harnessing computer power continue to drive composite manufacturing in aerospace. These include integrated computational materials engineering (ICME), which can leverage the flow of data among disparate model frameworks; digital manufacturing, giving rise to digital twins; and the use of analytics to bridge the growing gap between 3D-printed parts and certifiable validation of their integrity.

With ICME, aerospace manufacturers see the significant benefits of agility within frameworks that encompass entire organizations, including their customers and stakeholders. A focus on the flow of data to link these frameworks provides both actionable information and performance metrics across silos that can be applied, in theory, at any level in the organization. With their growing complexity, these legacy companies also recognize the critical role of the small business “hard tech” startup often five to 15 years in advance of their impact. This is especially true for material providers, where heavy R&D is often subsidized by government investment in recognition of its pivotal value later.

Composites are the ideal material systems to both drive and add value to modeling, analytics or digital twin approaches where the complexity in components, additives and their morphology give rise to innumerable performance differences not only in the choice of constituents, but the manufacturing process as well. This value is especially true when computation can significantly reduce the time between customer requirements and FAA certification.

The crossroads of emerging technologies with United States modernization priorities have been in hypersonics, the off-planet economy (space) and cyber security. The latter provides ample challenges for the entire aerospace supply chain, not the least being the need to protect information. Beginning Nov. 30, 2020, the U.S. Department of Defense (DOD) introduced a self-assessment methodology requiring the DOD supply chain to quantify and report their current cybersecurity compliance. On the innovation side, government agencies continue to promote collaboration between startup technology developers and Tier 1 aerospace companies. One example is the Air Force’s AFWERX program, which facilitates connections across industry, academia and the military.

Critical to these emerging technologies are advancements in materials. The need for materials that survive in the harshest of environments between Mach 5 and Mach 20 in space have led to an increase in additively manufactured ceramic matrix composites research and investment. To gain a stronger foothold in aerospace, the composites industry can use lessons learned in polymeric and metal matrix composites to inform model-driven design of ceramic matrix composites using ICME workflows. Additionally, converting expert knowledge into basic two-by-two orthogonal designs of experiment that compare the legacy material within the same experiment will build confidence around using new composite materials and manufacturing approaches.

While baseline metrics have historically included high strength-to-weight ratios, corrosion and chemical resistance, the new off-planet space economy calls for survivability in extreme hot and cold temperatures. Volunteering to contribute to standard development, such as the work being done by the American Institute of Aeronautics and Astronautics (AIAA) Standards Steering Committee (SSC), will help to normalize testing and other activities among aerospace stakeholders.

In conclusion, the future of aerospace depends more than ever on its ability to innovate. That will require integrated development among government, primes, supply chains and startup stakeholders. Every stakeholder will play a significant role in balancing compliance and business model disruption to ensure a rebound.

The Construction/Infrastructure Market

By Ken Simonson, Chief Economist, Associated General Contractors of America

Most construction firms are glad to close the books on 2020. But there is plenty of uncertainty as to whether 2021 will present more opportunities or continuing hardship.

At first appearance, construction held up relatively well in 2020. The value of construction put in place, seasonally adjusted, was nearly identical in October and February, the Census Bureau reported on Dec. 1, 2020. But peel back the top layer from that onion and differences poke out. Residential construction spending – new single- and multifamily construction and improvements to owner-occupied homes – increased 7%, while private nonresidential spending slumped 6% and public spending on projects under way slipped 2%.

As public works that began long before the pandemic finish up, public spending is likely to decline much more in 2021. Private nonresidential construction also appears likely to shrink further, at least in the first half of the year.

All types of owners have experienced revenue losses that may leave them unable to afford, or qualify for, financing for construction – businesses that had planned to expand or modernize; investors and developers of income-producing property; universities and other nonprofits; and state and local governments. Some owners will have shut down permanently, while many more will find the demand for additional facilities has disappeared or, at best, become too uncertain to justify starting construction in 2021.

In the near term, only a few nonresidential niches look promising. These include renovations of many types of existing facilities to accommodate coronavirus-related requirements or where a new tenant or user type replaces one that closed. The demand for “last mile” or “last hour” distribution facilities close to residential customers will remain strong, as will demand for more data centers. More facilities will be needed for delivering medical care, screening and testing outside of hospitals and nursing homes. Selected manufacturers will want to add capacity to meet surging demand for certain products. And a jump in homebuilding, some of it in undeveloped areas, will trigger limited demand for related infrastructure, retail, consumer services and local public facilities.

Most infrastructure and public building construction will be constrained by the balanced-budget mandates for nearly all state and local government entities, declines in tax and user-charge revenues and unbudgeted expenses related to the pandemic. The outlook will brighten slightly for 2021 if the federal government enacts substantial funding explicitly for infrastructure or to backfill revenue losses incurred by state and local governments generally or specific highway, transit or airport agencies. However, the lengthy process of distributing funds to agencies; allowing time for design, bidding and contract award; and assembly of equipment, materials and workers by the winning bidder means that most of the spending would occur after 2021.

School construction may be a partial exception. Much of the funding comes from property taxes, which have not declined nearly as much as sales or income taxes, let alone transportation user fees. Unlike passengers or vehicles, there has been no decline in the number of pupils once they can safely return to schools. As more families relocate, demand will grow for both new and renovated or expanded schools.

The pandemic has added to demand for ways of replacing scarce, onsite, skilled labor. To the extent that composite materials and products enable substitution of offsite fabrication, or quicker installation by smaller or less skilled crews, there will be growing demand for composites, even if the products themselves cost more.

Thus, 2021 is likely to be a challenging year for contractors. But it may mark a turning point for composites manufacturers hoping to crack the construction market.

Vectorply combines highly engineered composite reinforcements w/ industry-leading engineering & technical support to help customers achieve their production goals.

A lower-cost “print only” line of machines built around proven LSAM technology

More from Composites Magazine

SUBSCRIBE TO CM MAGAZINE

Composites Manufacturing Magazine is the official publication of the American Composites Manufacturers Association. Subscribe to get a free annual subscription to Composites Manufacturing Magazine and receive composites industry insights you can’t get anywhere else.